The purchase of a vehicle is a major financial decision. In 2016, the average new car price was an astonishing $33,666. If we break it down a bit further, the average price of a full-sized car was $34,505, a full-sized pickup truck was $46,332, and the average subcompact was $17,218.1 Regardless of which type of vehicle you are looking at, if you don’t have the cash on hand you will need to consider taking out a car loan.

In this article we will explore some of the best car loans available for Latinos, and highlight some things to look out for during the negotiation process. Our goal is to provide actionable information which can empower Latinos to find the best possible car loan available.

The Basics of Car Loans

If you are unfamiliar with the basic terminology of loans, take a look at this article we published before continuing with the rest of this article. This will help you “speak the language” as you begin your search for a car loan. Once you have these basics in mind, it is important to understand some car loan mechanics such as APR and the difference between a fixed and variable rate auto loan.

APR stands for Annual Percentage Rate and represents the annual cost of your loan. This figure is expressed as a percentage, and will be applied to the balance each month to determine how much interest is owed. According to Experian, the average APR for a fixed rate loan on a vehicle was 4.79% APR in 2016. 2 What APR you will receive will depend heavily on the type of vehicle you are purchasing, whether it is new or used, and what your credit score looks like.

A Fixed Rate Loan is a loan where the interest rate is fixed. If you get a 4.79% fixed rate loan today, you will be paying this same 4.79% interest rate in the final months of your loan - guaranteed.

A Variable Rate Loan is a loan where the interest rate can move based on two primary factors: The rate can change due to changes in the overall interest rate environment or the rate can change after a certain number of months have passed.

Regarding interest rates in the overall economy - interest rates are at historic lows, so the likelihood of a variable rate loan getting cheaper is also low. Regarding the passage of time, it is a common sales tactic for auto dealers to offer “super low introductory rates” which may go sky-high after the first 12 or 16 months. For both of these reasons, many Latinos prefer working with a fixed rate loan.

Some Places to Start Your Search

There are a number of financial institutions which are managed by, and built for, Latinos. One of them which we have mentioned on Super Moderno in the past is the Cooperativa Latina Credit Union. This firm, based on the East Coast, specializes in servicing and educating the Latino community. Below are their fixed auto loan rates as of 4/27/17. (Please Note: These may have changed after this date.)

| New Vehicle | Used Vehicle | |

|---|---|---|

| Loan to Value | 95% | 95% |

| APR | 5.75% | 8.25% |

| Max Amount | $60,000 | $60,000 |

| Average Payment | $411 | $441 |

This table highlights an important concept: you will be paying higher interest rates when getting a loan on a used vehicle than on a new vehicle. This is due to two primary factors:

-

Buyers with lower credit scores tend to purchase used vehicles, rather than new vehicles. Banks need to charge higher interest rates on used vehicle loans to accommodate for this.

-

New vehicle prices are more easy to predict. In the event that you can’t pay back your loan, the bank will take back the vehicle and sell it to recover their lost capital. The bank will have a pretty good idea of what a new car will be worth in one, three, or five years. It can be much more difficult to project the value of a used vehicle in one, three, or five years - especially if the vehicle is no longer under warranty.

Overall, these rates are relatively high compared to the national average, but there can be value in working with an organization that understands your family and the needs of the Latino community. Trust your gut, and keep in mind that the lowest rate may not always be the “best” rate.

The Big Banks

All major banks, like Wells Fargo or Bank of America, offer auto loan financing. If you aren’t set on working with a truly local organization, consider visiting your local branch of a nationwide banks. As always, it is critical to shop around and find the best rates available within your local market.

Dealer Financing

Here is the second way to get auto financing - directly through the dealership. This is called dealer financing and almost all vehicle showrooms will offer some type of financing to potential buyers. Especially when working with a used car dealership, it is critical to read the fine print. Historically, the used car financing market has had a reputation of using bait-and-switch tactics or offering low introductory rates which will go sky high after a period of time.

So, why do some Latinos opt for dealer financing? Well it can certainly simplify the process of buying a vehicle. Instead of contacting a bank, getting financing, then purchasing a vehicle - it is all done in one swift motion. Again, dealer financing has benefits and drawbacks, and there is not right fit for everyone. Before working with a dealer, keep reading to see what you should keep in mind.

What To Keep In Mind

Now that we have covered the basics of car loans, let’s explore some of the common traps to avoid. At Super Monedero, we want to not only provide basic information, but share our own experiences which can help you navigate the financial world.

Rates As Low As…

This is a common phrase used in auto loan advertising, and many times it is a rate which the average person walking into a dealership will not receive. In order to get this “rock bottom” rate, you will need to have an excellent credit score and are many times required to put 20% down on the vehicle purchase. For a $25,000 vehicle, this means putting $5,000 down the minute you purchase the new car. If you don’t have an excellent credit score or don’t have the cash on hand to make the down payment, it is likely that these “rates as low as…” will not apply to you.

Don’t get caught in a classic bait-and-switch tactic of contacting a dealership for an advertised rate and end up paying significantly more. For this reason, it’s important to understand how much cash you have on-hand and your credit score before you start the negotiation process.

Lower Rates, Longer Time Horizon

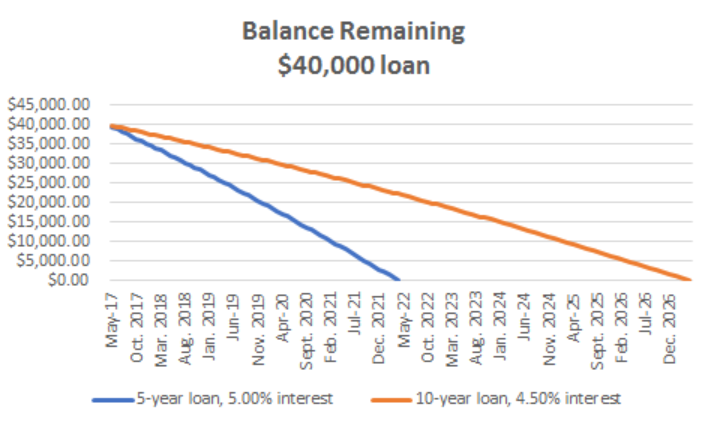

Specifically when working with a dealership on auto loan financing, it is important to crunch the numbers and determine exactly how much interest you will be paying under the terms of the loan agreement. It can be a common practice for dealerships to offer lower interest rates which come with longer time horizons for paying off the debt. In the end, you may be better off paying a higher interest rate over a shorter period of time on your auto loan. To illustrate this, consider two $40,000 car loans started in May of 2017.

The blue line represents a 5-year loan with a 5.00% interest rate while the orange line represents a 10-year loan with a 4.50% interest rate. In the financial world, 0.50% points on a loan is massive - so it is likely that the 10-year loan at 4.50% may look more attractive on face value. First of all, consider the fact that you will be paying this debt for five additional years. This is five years of debt payments which could be directed toward savings accounts, investment accounts, or a family vacation.

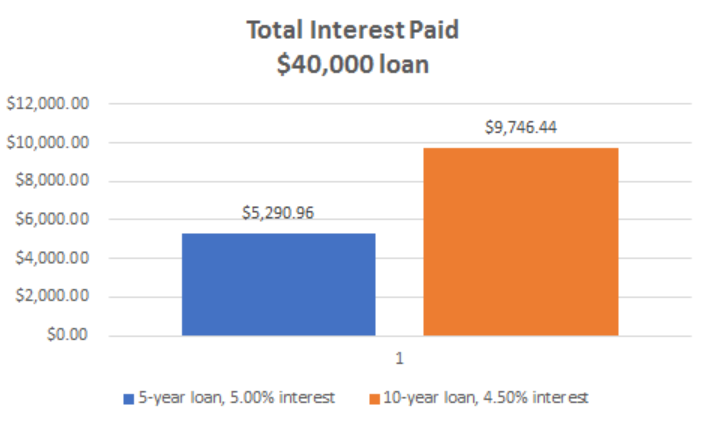

Second of all, and most importantly, is to consider the total interest paid on the loan. Due to the five year difference in loan duration, the 10-year loan requires $4,455.48 in additional interest payments.

As you can see, the 10-year, 4.50% loan, comes with significantly more interest paid over the life of the loan. This example does a good job of highlighting the fact that a loan which looks less attractive at face-value may actually be the best option for you and your family. The best way to know for certain? Crunch the numbers or ask the dealership for a loan amortization schedule. This document will show you when payments are due, how much of the payments go toward the principal amount, and what the total interest paid will be over the life of the loan.

Monthly Payments and Trade-Ins

Similar to our previous example, a common tactic used in the auto loan world is to put the focus on the monthly interest payment of the vehicle. By focusing on the monthly interest payment, you are missing the “big picture” and not considering the length you will be in the loan and the total interest paid over the life of the loan. This is especially true if you are trading-in a current vehicle, as the dealer can offer you an attractive monthly payment while offering you below market value for the trade in.

When looking to trade-in your current vehicle, consider the value of your current vehicle and the price of your new vehicle as two separate transactions. By doing this, you can maximize the sale price of your old vehicle and minimize the cost of your new vehicle - creating the most value for yourself in the transaction.

Final Thoughts

Second only to buying a home or taking out student debt, the purchase of a vehicle is one of the biggest financial decisions many Latinos will make. Take your time, crunch the numbers, and ask friends and family members what their experiences have been. At Super Monedero, we are with you every step of the way.